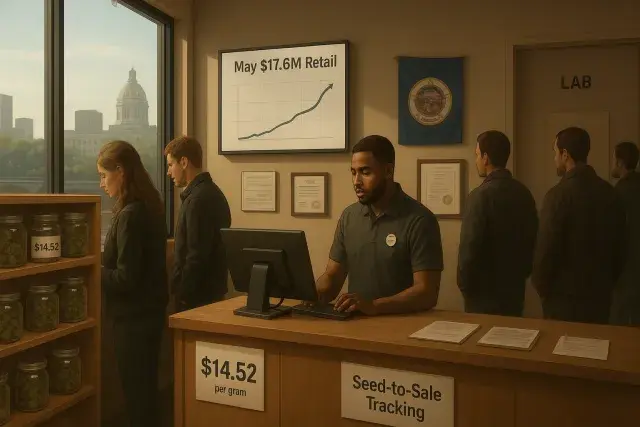

Minnesota's legal adult-use cannabis market posted $17.6 million in retail sales in May - roughly double what the state was generating when its first non-tribal dispensaries opened last fall. That's real momentum, and operators are right to mark it. But the number also tells a more complicated story about a market still constrained by thin inventory, a licensing pipeline that hasn't fully converted to open storefronts, and a testing infrastructure now under fresh strain.

The state has issued licenses to 153 retailers, though not all of them have opened - a gap that matters more than it might appear on the surface. Getting licensed is one thing; getting product on the shelves is another. Operators across newly legal markets routinely describe a lag between license approval and the first day of sales, driven by buildout timelines, local permitting, staffing, and - critically - the ability to source tested, compliant inventory at viable wholesale prices. Those same operational pressures have played out in other regulated markets. Retailers in states with POS-dependent compliance requirements, from Illinois to New Mexico, have found that managing seed-to-sale tracking and COA documentation at launch strains internal systems in ways that licensing prep never fully anticipates. Even in mature markets like Alaska, the sophistication of retail infrastructure - including cannabis pos software alaska adoption - reflects years of iteration that Minnesota's operators are only beginning.

What's striking here is where the supply pressure is actually coming from. One of Minnesota's few licensed testing facilities has lost its license and announced it's shutting down. That isn't just a compliance story - it's an inventory story. In every regulated cannabis market, lab testing sits in the critical path between cultivation and the sales floor. No COA, no sale. When lab capacity contracts, batches queue up, wholesale menus thin out, and retailers find themselves unable to build budroom inventory against rising consumer demand. The math isn't complicated: fewer testing slots means longer turnaround times, which means more product stuck in the pipeline waiting for results, which means dispensary shelves move slower than sales would otherwise support.

High Prices Signal a Market Not Yet in Equilibrium

The median retail price of a gram of flower in Minnesota sat at $14.52 in May. To put that in context: in mature, well-supplied adult-use markets, gram prices have compressed significantly as cultivation scale increased and wholesale competition intensified. Minnesota isn't there yet, and the testing bottleneck is one reason why.

High flower prices cut both ways for operators. Gross revenue looks better per transaction, but operators in early-stage markets consistently report that price is the primary reason legal-market consumers return to unregulated sources. That's a compliance and public-health problem as much as a competitive one - and it's exactly the dynamic regulators in every newly legal state have worked to prevent by building out testing capacity early. Minnesota, by that measure, is in a fragile moment. Experts widely expect prices to decline as supply normalizes, but "eventually" isn't a timeline that helps a retailer managing cash flow today.

The Gap Between Projections and Reality Is a Useful Signal

One cannabis law firm projected $550 million in first-year retail sales for Minnesota. Annualizing May's $17.6 million figure puts the state on a trajectory well short of that. Fair enough - early-market projections in cannabis are notorious for running ahead of reality. They tend to model demand without fully accounting for licensing delays, lab capacity, local opt-out provisions, and the friction involved in building a compliant retail supply chain from scratch.

That gap isn't a failure. It's a calibration. What it tells operators, investors, and vendors entering the Minnesota market is that the near-term opportunity is real but constrained - and that the businesses best positioned to grow are those capable of managing tight inventory, maintaining compliance documentation under pressure, and operating efficiently at lower sales volumes than originally modeled. Wholesale buyers should be watching the testing facility situation closely; any further contraction in lab capacity will extend SKU shortages and complicate purchase order planning.

What Operators Should Be Watching Right Now

The testing facility closure deserves more attention than it's received. A single lab exit in a state with limited testing infrastructure doesn't just slow down one operator - it redistributes the entire market's testing queue onto fewer facilities, each of which has finite throughput. Regulators pulling a lab license is a legitimate enforcement action, but the downstream effect on retail inventory is immediate and real. Minnesota's Office of Cannabis Management will need to prioritize expanding licensed lab capacity, or the supply backlog will persist well past the point where cultivation scale would otherwise have started easing price pressure.

For dispensary operators, the near-term operational priorities are clear: maintain strong relationships with multiple cultivators and processors, build in lead time on purchase orders to account for testing delays, and ensure that point-of-sale systems and compliance logs are current - regulators in early-stage markets tend to audit more frequently as the industry scales. The 153-license figure will eventually translate to 153 open storefronts. When that happens, the competitive pressure on thinly stocked operators will intensify. Getting supply chain relationships right now, while the market is still forming, is worth more than any single month of headline revenue.