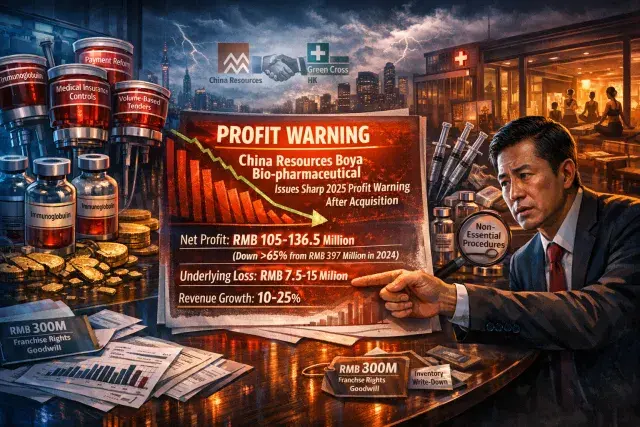

China Resources Boya Bio-pharmaceutical, a key player in blood products and medical aesthetics, has warned of a steep profit drop for 2025, projecting net profit attributable to shareholders at RMB105 million to RMB136.5 million—down over 65% from RMB397 million in 2024. This comes despite expected revenue growth, highlighting intensifying pressures in China's biopharma sector that could signal wider challenges for specialty drug makers.

Key Details of the Profit Slump

The company's announcement reveals a stark underlying net loss of RMB7.5 million to RMB15 million when stripping out non-recurring gains like government subsidies and investment income, which are forecasted to add about RMB120 million. Operating revenue should still climb 10% to 25%, fueled by the recent acquisition of Green Cross HK Holdings in November 2024.

- Net profit forecast: RMB105-136.5 million (vs. RMB397 million prior year)

- Underlying loss: RMB7.5-15 million (excluding one-offs)

- Revenue growth: 10-25%, acquisition-driven

Root Causes: Aesthetics Downturn and Acquisition Costs

Management pins the decline mainly on a cooling hyaluronic acid (HA) medical aesthetics market, prompting RMB300 million in impairments on franchise rights and goodwill from the Green Cross deal. Additional hits include RMB80 million from inventory revaluation, plus elevated depreciation and amortization. The HA sector, booming during the pandemic for fillers and skin boosters, now faces oversupply, regulatory scrutiny on non-essential beauty procedures, and shifting consumer priorities toward wellness over invasive tweaks—trends eroding demand across Asia.

Pressures on Blood Products Business

CR Boya's core blood products segment, vital for plasma-derived therapies like immunoglobulins, is squeezed by China's centralized procurement policies, payment reforms, stricter medical insurance controls, and fierce competition. These volume-based tenders slash prices and margins, a common plight for biopharma firms navigating the nation's healthcare cost-containment drive. Gross margins have eroded as hospitals favor low-bid suppliers, underscoring how policy shifts prioritize affordability over profitability.

Implications and Outlook for Chinese Biopharma

This warning spotlights vulnerabilities for China Resources Pharmaceutical's subsidiaries amid economic headwinds and regulatory tightening. While the Green Cross buy bolsters HA capabilities long-term, near-term pain from integration and market softness raises risks. Investors may eye cost controls and pipeline diversification into high-margin biologics. Broader trends—like aging populations boosting blood product needs but tempered by procurement—suggest CR Boya must adapt swiftly to sustain growth in a maturing market projected to favor innovators over incumbents.